I've built my reputation on turning complex market shifts into real opportunities for my clients—whether you're a first-time homebuyer navigating Alberta's dynamic housing scene, an investor eyeing seminar-worthy deals, or someone refinancing to free up cash flow. I'm here to demystify the latest interest rate landscape. If the Bank of Canada (BoC) delivers another cut on October 29, 2025, as many experts anticipate, it could supercharge affordability and put more Albertans into their dream homes. Let's dive deep into what these rates mean for you, backed by data, real-world examples, and actionable strategies to position you ahead of the curve.

The Bank of Canada's Role: A Quick Primer on How Rates Are Set

To truly grasp the impact, it's essential to understand the mechanics. The BoC's policy rate—also known as the overnight rate—is the benchmark that influences everything from your mortgage to credit card interest. It's set eight times a year to balance inflation (targeted at 2%) and economic growth. When inflation cools or the economy faces headwinds like global trade tensions or supply chain disruptions, the BoC cuts rates to stimulate borrowing and spending. Conversely, hikes curb overheating.

Historically, we've seen dramatic swings: Rates plummeted to near-zero during the pandemic to fuel recovery, then surged to combat post-COVID inflation, peaking at 5% in 2023. Fast-forward to 2025, and we're in a easing cycle. On September 17, 2025, the BoC slashed its rate by 25 basis points (0.25%) to 2.5%, resuming cuts after a brief pause earlier in the year. This move was driven by moderating inflation (now hovering around 2.1%) and softening labor markets, with unemployment ticking up to 6.6% nationally. In Alberta, where oil prices and energy sector volatility play a big role, these cuts provide a much-needed buffer against economic uncertainties like potential U.S. tariffs on Canadian exports.

Current Trends and Predictions: Where Rates Are Headed Next

As of mid-October 2025, the BoC's policy rate stands at 2.5%. Experts from RBC and others forecast another 25 basis point cut at the upcoming October 29 announcement, potentially dropping it to 2.25%. This aligns with broader trends: Bond yields, which heavily influence fixed mortgage rates, have been declining, reflecting market confidence in continued easing.

On the mortgage front, rates are already reflecting this optimism:

Variable Rates: Tied directly to the BoC's policy rate (often prime minus a discount), the lowest 5-year variable rates are around 3.6% to 3.75% from competitive lenders. With prime rates at major banks like RBC and TD sitting at about 4.7% to 4.85%, expect these to drop further post-cut.

Fixed Rates: More stable and influenced by government bond yields, 5-year fixed rates start as low as 3.84% for well-qualified borrowers, with averages around 4.49% to 4.59%. Shorter terms like 3-year fixed can dip to 3.79%.

In Alberta, particularly Calgary, we're seeing even more competitive offerings due to lower provincial regulations and a robust lender market. For instance, local brokers (like myself) can often secure rates 0.10% to 0.20% below national averages, thanks to volume discounts and relationships with over 40 lenders. Home prices here are stabilizing after a 2024 surge, with average detached homes in Calgary around $650,000—making now an ideal entry point before potential rate-driven demand spikes.

Looking ahead to 2026, optimistic forecasts suggest fixed rates could settle around 4.2% by year-end if cuts continue, while variables might hover near 3%. But remember, global factors like U.S. Federal Reserve moves or oil price fluctuations could alter this trajectory. That's why I monitor these daily via my CRM dashboards and share updates at investment seminars—helping clients pivot quickly.

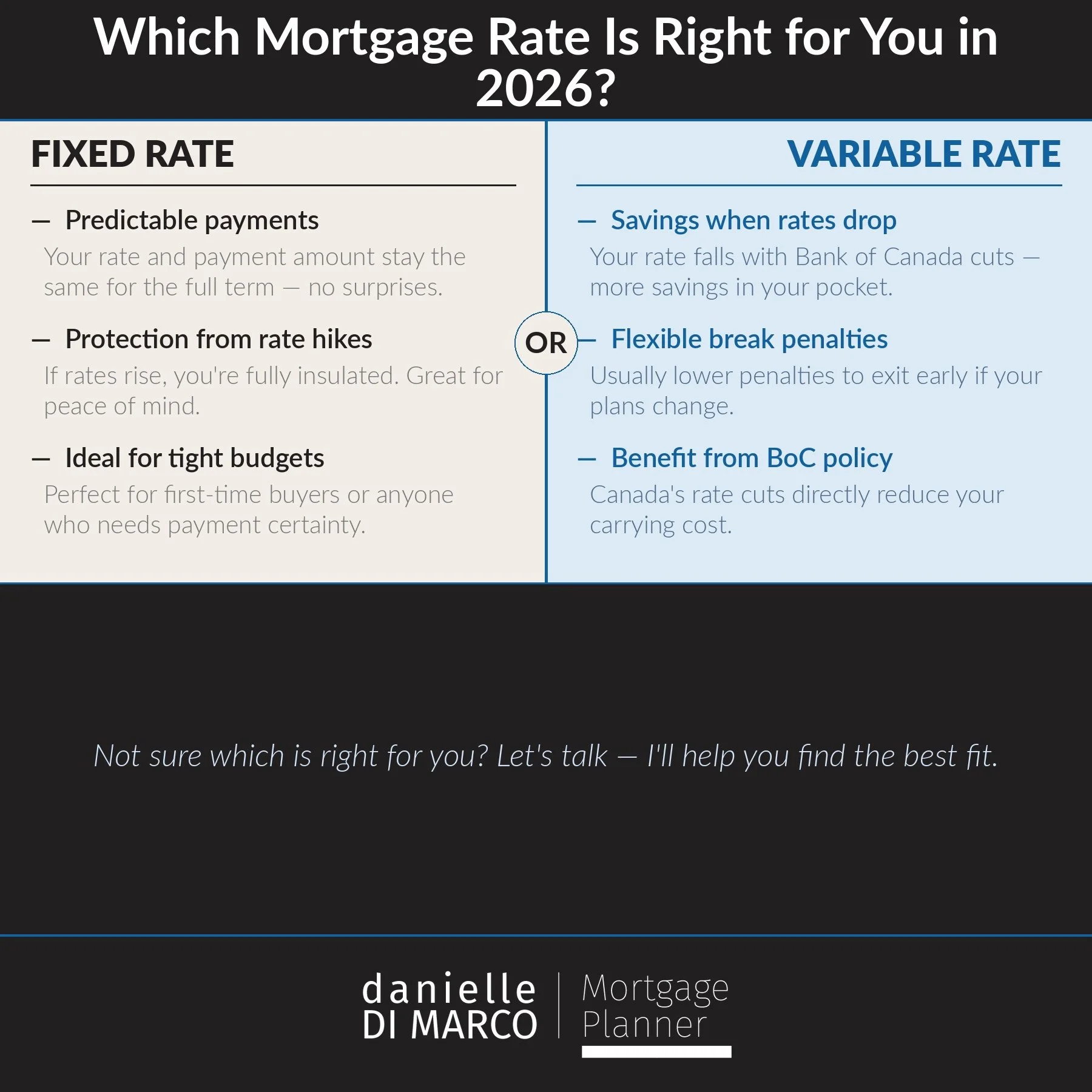

Variable vs. Fixed: Which Is Right for You in This Environment?

This is a hot topic at my seminars: Variable rates shine in falling environments, offering lower starts and penalty-free adjustments, but they carry risk if rates rebound. Fixed rates provide peace of mind with predictable payments, ideal for budget-conscious families.

In 2025's easing cycle, variables are winning for aggressive buyers—saving 0.5% to 1% upfront. But with Alberta's economy tied to volatile commodities, I often recommend fixed for stability, especially if you're in oil & gas. A client story: Last year, I switched a young family from a 5.5% variable to a 4.2% fixed just before hikes paused—saving them $15,000 annually. Testimonials like theirs fuel my drive to make you the smartest borrower in Calgary.

Alberta's Edge: Why Calgary Buyers Are Positioned to Win

Alberta stands out with no land transfer tax on new builds (unlike Ontario's hefty fees) and competitive inventory. Calgary's market is rebounding: Sales up 5% year-over-year, with prices expected to rise modestly by 3-4% in 2026 as rates ease. Factors like migration from pricier provinces and energy sector recovery add tailwinds. But challenges persist—tight supply in desirable neighborhoods means acting fast.

As your local expert, I pre-approve clients in hours, not days, and negotiate no-games rates upfront. Whether you're upsizing in the suburbs or investing downtown, timing around the October 29 announcement could be key—lock in now to avoid post-cut rushes.

Actionable Tips to Capitalize on These Rates

Get Pre-Approved: Secure your rate hold for 120 days—protect against surprises.

Stress Test Smartly: Even at lower rates, qualify based on 5.25% (the benchmark)—I run scenarios to maximize your approval.

Refinance Check: If your renewal is within 6 months, explore breaks—savings often outweigh penalties.

Diversify: Pair your mortgage with real estate investment strategies for long-term wealth.

Stay Informed: Follow me on Instagram for live updates, or subscribe to my newsletter via my website.

I thrive on transforming rate volatility into client wins. Ready to lock in Calgary's best rates and become the envy of your network? Contact me today for a free, no-obligation consultation—let's craft your personalized mortgage strategy and make you the best-prepared buyer in Alberta.