Canada's Economic Pulse: What March Economic Data Means for Your Mortgage

/

Trade deficits, building permits, and a bond market shock - here's what three big data releases mean for Calgary homebuyers and borrowers in 2026.

Read MoreTrade deficits, building permits, and a bond market shock - here's what three big data releases mean for Calgary homebuyers and borrowers in 2026.

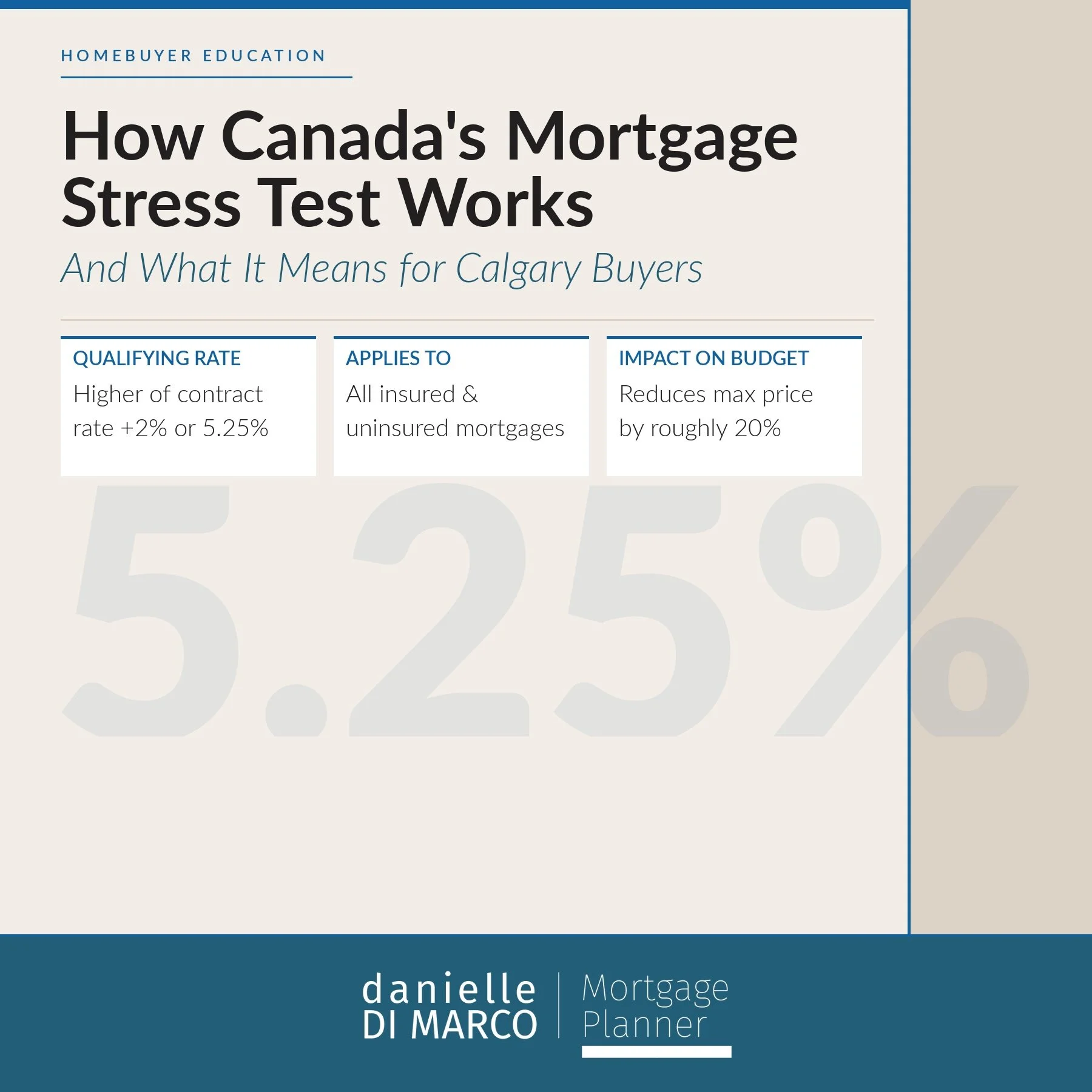

Read MoreCanada's mortgage stress test affects how much home you can afford. A Calgary mortgage broker explains the rules, the math, and how to maximize your buying power in Alberta.

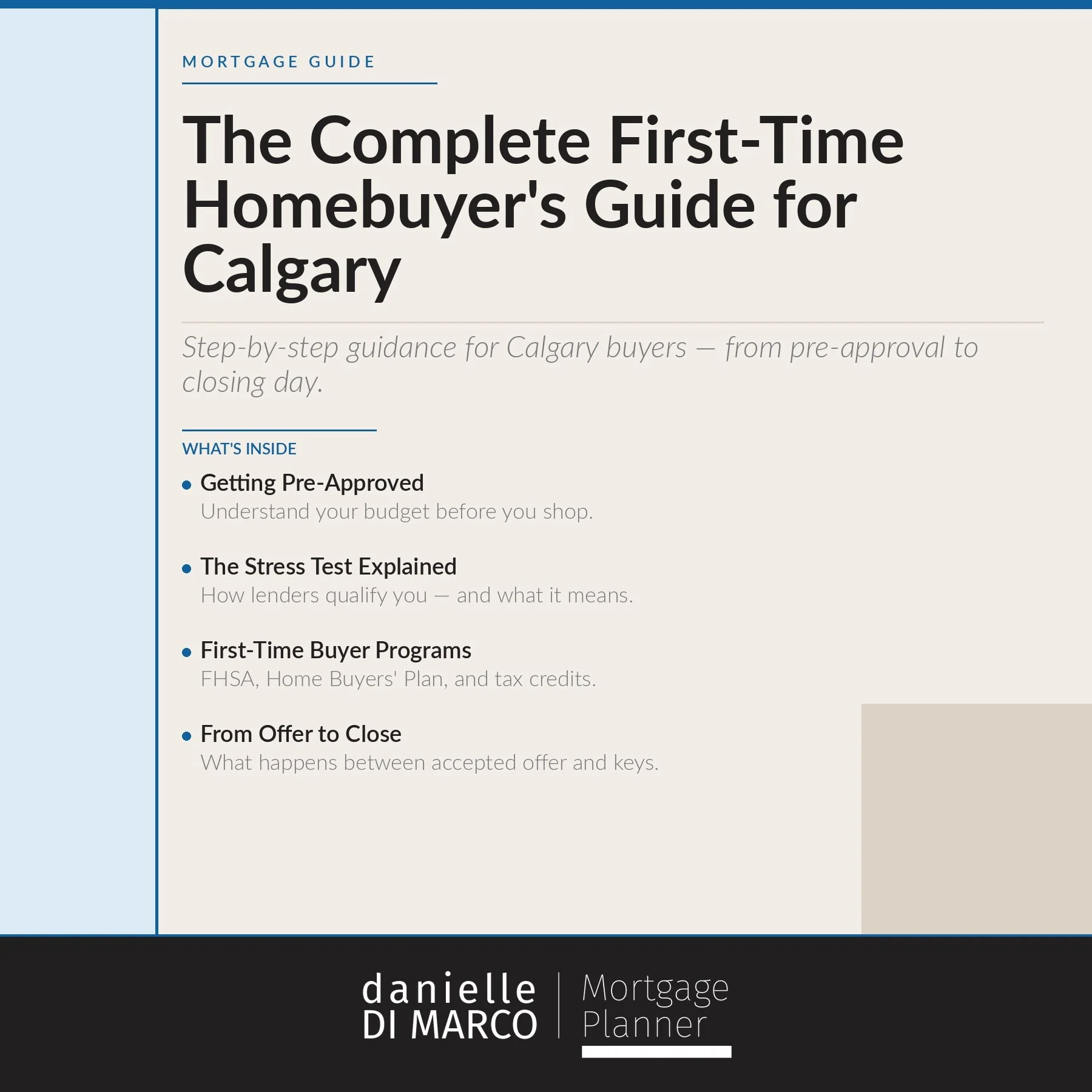

Read MoreEverything Calgary first-time homebuyers need to know — from mortgage pre-approval to closing day. Expert advice from a top-1% Calgary mortgage broker with 20 years experience

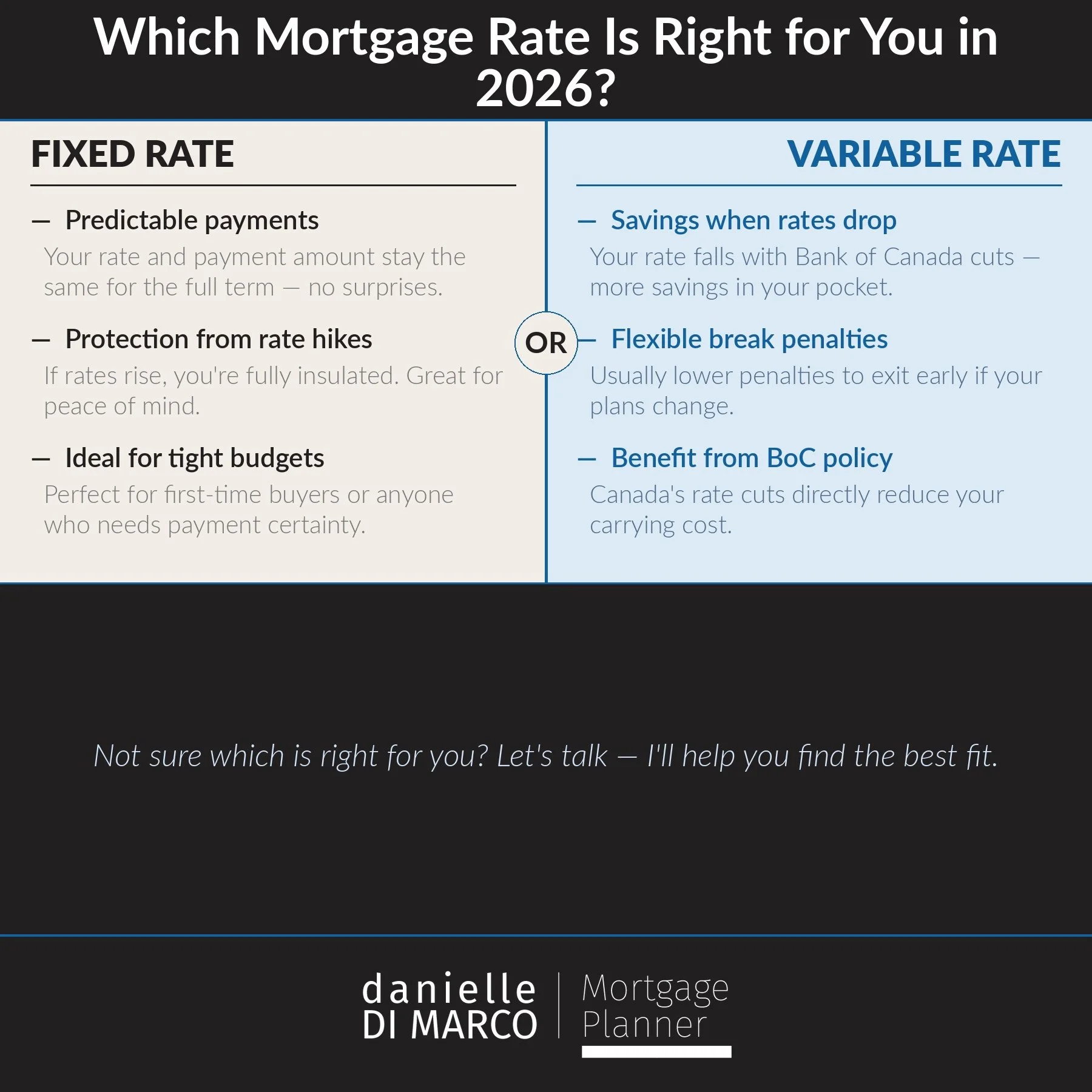

Read MoreNot sure whether to choose a fixed or variable mortgage rate? A top Calgary mortgage broker explains the differences, the risks, and how to decide what's right for your situation in 2026.

Read MoreI've built my reputation on turning complex market shifts into real opportunities for my clients—whether you're a first-time homebuyer navigating Alberta's dynamic housing scene, an investor eyeing seminar-worthy deals, or someone refinancing to free up cash flow. I'm here to demystify the latest interest rate landscape. If the Bank of Canada (BoC) delivers another cut on October 29, 2025, as many experts anticipate, it could supercharge affordability and put more Albertans into their dream homes. Let's dive deep into what these rates mean for you, backed by data, real-world examples, and actionable strategies to position you ahead of the curve.

To truly grasp the impact, it's essential to understand the mechanics. The BoC's policy rate—also known as the overnight rate—is the benchmark that influences everything from your mortgage to credit card interest. It's set eight times a year to balance inflation (targeted at 2%) and economic growth. When inflation cools or the economy faces headwinds like global trade tensions or supply chain disruptions, the BoC cuts rates to stimulate borrowing and spending. Conversely, hikes curb overheating.

Historically, we've seen dramatic swings: Rates plummeted to near-zero during the pandemic to fuel recovery, then surged to combat post-COVID inflation, peaking at 5% in 2023. Fast-forward to 2025, and we're in a easing cycle. On September 17, 2025, the BoC slashed its rate by 25 basis points (0.25%) to 2.5%, resuming cuts after a brief pause earlier in the year. This move was driven by moderating inflation (now hovering around 2.1%) and softening labor markets, with unemployment ticking up to 6.6% nationally. In Alberta, where oil prices and energy sector volatility play a big role, these cuts provide a much-needed buffer against economic uncertainties like potential U.S. tariffs on Canadian exports.

As of mid-October 2025, the BoC's policy rate stands at 2.5%. Experts from RBC and others forecast another 25 basis point cut at the upcoming October 29 announcement, potentially dropping it to 2.25%. This aligns with broader trends: Bond yields, which heavily influence fixed mortgage rates, have been declining, reflecting market confidence in continued easing.

On the mortgage front, rates are already reflecting this optimism:

Variable Rates: Tied directly to the BoC's policy rate (often prime minus a discount), the lowest 5-year variable rates are around 3.6% to 3.75% from competitive lenders. With prime rates at major banks like RBC and TD sitting at about 4.7% to 4.85%, expect these to drop further post-cut.

Fixed Rates: More stable and influenced by government bond yields, 5-year fixed rates start as low as 3.84% for well-qualified borrowers, with averages around 4.49% to 4.59%. Shorter terms like 3-year fixed can dip to 3.79%.

In Alberta, particularly Calgary, we're seeing even more competitive offerings due to lower provincial regulations and a robust lender market. For instance, local brokers (like myself) can often secure rates 0.10% to 0.20% below national averages, thanks to volume discounts and relationships with over 40 lenders. Home prices here are stabilizing after a 2024 surge, with average detached homes in Calgary around $650,000—making now an ideal entry point before potential rate-driven demand spikes.

Looking ahead to 2026, optimistic forecasts suggest fixed rates could settle around 4.2% by year-end if cuts continue, while variables might hover near 3%. But remember, global factors like U.S. Federal Reserve moves or oil price fluctuations could alter this trajectory. That's why I monitor these daily via my CRM dashboards and share updates at investment seminars—helping clients pivot quickly.

This is a hot topic at my seminars: Variable rates shine in falling environments, offering lower starts and penalty-free adjustments, but they carry risk if rates rebound. Fixed rates provide peace of mind with predictable payments, ideal for budget-conscious families.

In 2025's easing cycle, variables are winning for aggressive buyers—saving 0.5% to 1% upfront. But with Alberta's economy tied to volatile commodities, I often recommend fixed for stability, especially if you're in oil & gas. A client story: Last year, I switched a young family from a 5.5% variable to a 4.2% fixed just before hikes paused—saving them $15,000 annually. Testimonials like theirs fuel my drive to make you the smartest borrower in Calgary.

Alberta stands out with no land transfer tax on new builds (unlike Ontario's hefty fees) and competitive inventory. Calgary's market is rebounding: Sales up 5% year-over-year, with prices expected to rise modestly by 3-4% in 2026 as rates ease. Factors like migration from pricier provinces and energy sector recovery add tailwinds. But challenges persist—tight supply in desirable neighborhoods means acting fast.

As your local expert, I pre-approve clients in hours, not days, and negotiate no-games rates upfront. Whether you're upsizing in the suburbs or investing downtown, timing around the October 29 announcement could be key—lock in now to avoid post-cut rushes.

Get Pre-Approved: Secure your rate hold for 120 days—protect against surprises.

Stress Test Smartly: Even at lower rates, qualify based on 5.25% (the benchmark)—I run scenarios to maximize your approval.

Refinance Check: If your renewal is within 6 months, explore breaks—savings often outweigh penalties.

Diversify: Pair your mortgage with real estate investment strategies for long-term wealth.

Stay Informed: Follow me on Instagram for live updates, or subscribe to my newsletter via my website.

I thrive on transforming rate volatility into client wins. Ready to lock in Calgary's best rates and become the envy of your network? Contact me today for a free, no-obligation consultation—let's craft your personalized mortgage strategy and make you the best-prepared buyer in Alberta.

Picture this: It's mid-October 2025, leaves are turning, and your mailbox finally arrives—that renewal notice from your bank. If you're one of the 1.2 million Canadians staring down a mortgage renewal this year, I get it; the knot in your stomach is real. After 13+ years brokering deals that prioritize your peace of mind, I've walked countless families through this exact moment. The truth? With rates at multi-year lows and smart strategies in play, this "wave" doesn't have to drown you. Let's unpack it together, step by step.

Flash back to 2020: Rates were sub-1%, fueling a buying boom. Fast-forward to now, and those ultra-low deals are expiring against a backdrop of 2.5% policy rates and lingering tariff effects. CMHC data shows 85% of fixed-rate mortgages from that era renew this year or next, with average payments jumping 10%—that's $400-600 more monthly for a $400,000 loan.

But hold on—it's not all doom. The Bank's easing cycle has variable primes at 4.7%, and delinquency rates are still a whisper at 0.23% (up slightly from last year, thanks to unemployment edging to 6.8%). Equifax reports 28% of renewers are switching lenders for better deals, a 46% jump from 2024. Why? Because banks aren't always your best friend at renewal; they bank on loyalty.

In my Calgary practice, I've seen local impacts firsthand: Oil sector layoffs from U.S. tariffs mean tighter budgets, but Alberta's steady home prices ($520,000 median) and rising inventory give leverage. Nationally, CREA forecasts a 6% sales rebound in 2025, driven by these renewals shaking loose sellers.

This is where I shine—cutting through the noise to match your vibe. Fixed rates? They're your steady eddy, around 4.1-4.4% for five years, shielding you from hikes if tariffs reignite inflation (forecasts see CPI at 2.1% by 2026). Variable? At 3.6-3.85%, they're cheaper now, with experts like TD Economics predicting another 25 bps cut to 2.25% by Q4. But if job markets wobble, payments could flex up 5-10%.

Pro tip from the trenches: If your budget's ironclad (under 30% of income on housing), go variable for potential savings—could shave $5,000 off interest over five years. Otherwise, fixed it is. And don't sleep on shorter terms: A three-year at 3.9% lets you reassess in 2028 when forecasts show stabilization.

You deserve transparency, so here's my no-BS playbook—tailored for real families, not spreadsheets:

Renewal letters come 3-6 months early, but start sooner. I'll pull rates from 20+ lenders (no cost to you) and guarantee the best upfront—no bait-and-switch.

Got home equity? Tap it tariff-proof: Consolidate high-interest debt at 4.5% vs. 19% credit cards. Saves hundreds monthly.

Extending amortization to 30 years lowers payments $200-300, but it amps total interest. We model it out to keep you on track for payoff.

Renewals coincide with holidays—budget for that. And with food insecurity up 15% amid tariffs, build a $3,000 emergency fund first.

Skip bank advisors; brokers like me work for you. We've closed 95% of renewals on time, with clients saving an average 0.4% on rates.

Renewals feel big, but they're your pivot point. With home prices up just 2% nationally and more listings, you're positioned to refinance into a bigger space or downsize for cash. I've seen clients turn $500 payment hikes into $1,200 annual savings by switching—pure win.

You're in the know now, and that's half the battle. Ready to map your renewal? Shoot me a message—let's make it smooth, savings-packed, and stress-free. You've built this equity; now let's protect it.

What's your renewal timeline? Share below—community chats keep us all ahead.

Hey there, if you're anything like the hundreds of clients I chat with every year, you've been keeping a close eye on those Bank of Canada announcements. Just last month, on September 17, 2025, they dropped the overnight rate by another 25 basis points to 2.5%—that's the seventh cut since June 2024, and it's got everyone talking. As someone who's helped Calgary families close on time and lock in the best rates for over 13 years, I can tell you this: lower rates aren't just numbers on a screen; they're a real shot at making homeownership a little less stressful in this unpredictable economy.

The Bank of Canada's policy rate is like the heartbeat of our lending world—it influences everything from your variable mortgage payments to what banks charge for fixed terms. At 2.5%, the prime rate has dipped to 4.7%, which means variable rates are now hovering around 3.6% for a five-year term (the lowest I've seen in months). Fixed rates? They're holding steady in the low 4% range, but with bond yields cooling off, we could see them nudge down to 4.2% by year's end.

This isn't happening in a vacuum, though. We're still feeling the ripples from U.S. tariffs that kicked in earlier this year—think higher costs for everything from lumber to auto parts, which nudged inflation up to 2.3% in August. The Bank's move is their way of saying, "We're supporting growth while keeping prices in check." For you, that translates to more breathing room on your monthly budget. Take a $500,000 mortgage on a 25-year amortization: at 4.7% prime, your variable payment drops about $125 a month compared to pre-cut levels. That's real money back in your pocket for groceries or that family vacation.

But here's the flip side—and I always keep it real with my clients: unemployment ticked up to 6.8% last quarter, and with over 1 million renewals hitting in 2025, not everyone will feel the full relief. If you're renewing from those rock-bottom 1% rates of 2020-2021, expect a bump—maybe $300-500 more per month on average. The good news? Stress tests are still protecting lenders, so defaults remain low at 0.21%.

I've seen markets swing before, and right now, the Canadian Real Estate Association reports sales up 1% nationally in September—small, but it's the fifth month in a row of gains. Prices climbed 2% year-over-year to around $697,000, but with more inventory in places like Calgary and Toronto, it's tilting toward buyers. Lower rates are unlocking pent-up demand; we saw a 20% spike in inquiries right after the announcement.

In Alberta, where energy exports took a hit from tariffs, affordability is improving—median homes here are still under $550,000, and with rates easing, first-time buyers are jumping back in. But watch Ontario and B.C.: backlogs of unsold condos could keep prices flat through winter.

Your Action Plan: Three Steps to Make These Rates Work for You

Banks love to offer their "standard" rates, which are often 0.5-1% higher than what brokers like me can secure. With renewals flooding in, compare fixed vs. variable now. If you're risk-averse, lock in a five-year fixed at 4.1%; if you can handle some flux, variable could save you thousands if cuts continue (forecasts point to 2.25% by December).

Use a simple calculator (I can walk you through one) to see how a 0.25% drop affects your payments. Factor in tariffs' sneaky inflation—groceries up 3% last month means padding that buffer. And if you're buying, the new 30-year amortization for first-timers (from December 2024 rules) just stretched your buying power by 10%.

Opt for a mortgage with a 20% prepayment privilege—lets you pay down principal faster without penalties. Or consider a hybrid: fixed for stability, variable for the savings. I've helped clients blend these to close gaps from job shifts in this tariff-tough economy.

Lower rates are a welcome breather, but with economic curveballs like trade tensions, the key is staying informed and proactive. I've got your back—whether it's decoding a pre-approval or negotiating that rate hold. Drop me a line, and let's chat about your next move. Because when you close on time and with the best deal, that's when the real celebrating starts.

What are your thoughts on this cut? Hit reply or connect on social—I'm here to help.

My name is Danielle Di Marco, and I am your trusted Calgary Mortgage Broker! I treat every mortgage solution as if I'm constructing your dream home - the solution I recommend for you will be designed for you specifically; carefully constructed to match your unique requirements. After all, this is one of the biggest financial decisions you may ever make.

I am always working to raise the bar on my services. If you have any questions or concerns, please let me know.

Danielle Di Marco

403.969.0233

danielle@danielledimarco.com